Chitty Chitty Bang Bang is a 1968 children’s film that I loved catching on television during the 1970s. Given that it is a children’s fantasy musical starring Dick Van Dyke with songs by the Sherman Brothers, you might think it was by Disney. But the gimmicky car is the giveaway that the movie was produced by Albert Broccoli, one of the creators of the James Bond movie franchise.

The original story was actually by Ian Fleming, the author of the Bond novels. Fleming had a heart attack in 1961 and decided to write a children’s novel based on stories about a flying car he once told his infant son. He wrote the book in longhand since his wife, in a vain attempt to get him to rest, had confiscated his typewriter.

The novel was released in installments from October 1964 to January 1965, a few months after Fleming’s death. 1964’s Mary Poppins was a huge hit for Walt Disney, featuring Julie Andrews and Dick Van Dyke, with songs by the talented Robert and Richard Sherman. They would go on to write more movie musical song scores than any other team in history, including later works like Bedknobs and Broomsticks, The Jungle Book, and Charlotte’s Web.

The success of Poppins convinced Broccoli to produce a film version of Chitty Chitty Bang Bang. He tried to cast both Andrews and Van Dyke, but Andrews declined and instead Sally Ann Howes played the female lead. Broccoli convinced Disney to release the Sherman Brothers from their contract so they could compose the songs for his film, which included a beautiful but melancholy ballad, Hushabye Mountain.

Dick Van Dyke sang it in the movie, in an orchestral arrangement by Irwin Kostal.

National treasure Tony Bennett released a version before the film was even released, but the real treat is to watch him sing it live.

The song has been covered by many artists over the decades, but here is a clip in which the creators of the song, the Sherman Brothers, perform a bit of it.

We lost Robert Sherman in 2012 and Richard in May 2024. A famous story about them was how Walt Disney’s favorite song was their Feed the Birds from Poppins. Walt would often invite the brothers to his office after work on Fridays and, after discussing work at the studio, wander to a window, look into the distance, and just say, “Play it.” Richard would go to the piano and play the song. One time, as the song was ending, they heard Disney say under his breath, “Yep. That’s what it’s all about.”

The Sherman brothers wrote many great songs, with half of the songs from Mary Poppins becoming standards. I will forgive them for the lengthy earworm It’s a Small World, which they wrote as a slow ballad but Walt had them play uptempo in counterpoint for the eponymous ride in Disney’s amusement parks.

Richard shared in a 2014 interview that Hushabye Mountain is one of his favorite songs. I concur, although it often makes me tear up.

For me, one of the most interesting covers of the song is on the last album by torch singer Julie London. I grew up seeing her on the paramedic television drama Emergency! in the 1970s, where she played Nurse Dixie. Julie and her husband in real life, jazz composer and singer Bobby Troup, were cast in the show by Julie’s ex-husband, Jack Webb of Dragnet fame. As for Troup, he famously composed (Get Your Kicks on) Route 66.

Here’s Julie’s take on the Sherman Brothers classic.

A gentle breeze from Hushabye Mountain Softly blows o'er Lullaby Bay It fills the sails of boats that are waiting Waiting to sail your worries away

It isn't far to Hushabye Mountain And your boat waits down by the quay The winds of night so softly are sighing Soon they will fly your troubles to sea

So close your eyes on Hushabye Mountain Wave goodbye to cares of the day And watch your boat from Hushabye Mountain Sail far away from Lullaby Bay

Robert and Richard, rest in peace on Hushabye Mountain.

How often do you still use cash? Do you still write some checks? Did you notice credit cards are no longer issued with raised numbers for imprinters? Do you even know what an imprinter is? Do you or should you tap to pay? How we pay for things continues to evolve, and the pandemic accelerated several trends.

The Decline of Personal Checks

It made news when Target stopped accepting personal checks in July 2024, but Aldi, Whole Foods, Old Navy, and Gap had stopped accepting them a decade earlier. While checks have been around for centuries, they are slow, cumbersome, and prone to fraud compared to other payment methods. The average American was writing over sixty checks a year in 2000, but by 2024 that had fallen to less than ten.

Back in the day, schoolchildren would go on field trips to a bank and learn how to write and use a check.

Schoolchildren visit a bank in Bartlesville in 1969

In my case, we rode a school bus to Fidelity Bank’s new tower in downtown Oklahoma City, completed a couple of years earlier in 1972 as part of urban renewal. I remember sitting in a large white room with high ceilings and tall windows as they went over banking procedures, including showing us how to write a check. My mother worked for years at a savings and loan, so I already knew all about that stuff.

My father worked for Cities Service Gas in the First National Bank’s skyscraper a few blocks away. One of my favorite things when visiting his building in the 1970s was to ride the escalator up into its tremendous marble banking hall. The hall is still there, but now refurbished into a restaurant and event space.

The amazing Banking Hall at OKC’s First National

Jack Conn

At the time, Fidelity was run by Jack Conn, who spearheaded the Conncourse system of underground tunnels connecting buildings across downtown OKC. It is now known as the Underground with a mile of tunnels that cover more than 20 square blocks.

George Kaiser’s Bank of Oklahoma merged with Fidelity bank in the 1980s oil bust, and I see that Arvest bank took over the former Fidelity/BOK tower in downtown OKC back in 2019. I’ve banked with Arvest, which is owned by the Walton family of Wal-Mart fame, for thirty years.

When I came to Bartlesville in 1989, I opened checking and savings accounts with WestStar, the major local bank at the time, which had begun in 1900 as Frank Phillips’ First National Bank of Bartlesville. In 1994, the Waltons bought out WestStar for $470 million. While I still have around 20 transactions in my checking account each month, I only write one or two checks annually. I’ve heard that fewer and fewer people even know how to properly write a check.

What Took Their Place?

Years ago I started eliminating having to write and mail in personal checks for household utilities. I signed up to have those charges deducted automatically from my checking account. I later started having home and automobile insurance deducted from my checking account as well, although I still write the occasional check for a specialized service like tree removal or fence installation.

The Federal Reserve has released its 2024 Findings from the Diary of Consumer Payment Choice, giving us some insights into the shifts in payment methods. Below are the shares of payment instrument use for all payments each year from 2016 to 2023.

Over those eight years, the share of payments handled via personal check dropped by more than half and cash transactions almost halved. Debit transactions increased by 11%, and credit card payments increased by 78%. ACH refers to electronic money transfers between banks and credit unions across the Automated Clearing House network, and those are up 30%. I generate an ACH each month since the school district direct deposits my pay into my Arvest checking account, and I transfer some of that to another bank for my long-term savings since their interest rates are higher.

Cash

For three consecutive years, consumers have reported making an average of seven cash payments per month, so it appears to have a “floor” level. When consumers are asked which payment method they prefer for in-person payments, there has been a significant shift from cash to credit.

That, along with a continuing shift from in-person purchases to online and remote ones, is helping keep the number of cash transactions steady even as the total number of transactions increases post-pandemic.

I should add that the type of payments one makes is correlated to household income. As income increases, the share of transactions done with cash declines in favor of credit cards.

I’ve experienced that myself, with Wendy routinely sending me money via Venmo when she charges something via an app on her iPad.

Credit Cards

Old-style store credit cards had no magnetic strip, just embossed numbers and a name for an imprinter

Back in 1970, when I was a kid, only 16% of U.S. families had a bank-type credit card. However, 45% had a retail store card. I recall that my mother had specific credit cards for Sears and J.C. Penney. The latter seemed ironic since she remembered how Penney’s was a cash-and-carry operation until 1958, originally promoting their lack of store credit as a way for consumers to avoid building up debt.

Mom kept using the same cards for decades. They had no expiration date and no magnetic strip, just embossed numbers and her name.

Credit card imprinters of yesteryear

Eventually when she would hand her card over, the clerk would pause, comment on how old the card was, and would have to reach under the counter to pull out an old manual imprinter since the card couldn’t be scanned by the register. They would place the carbonized sales slip and the card in the device and either pull down a lever or slide a bar back and forth to create an impression of the embossed card data.

Finally, sometime in the 21st century, the stores forced Mom to give up her old cards, replacing them with modern ones with magnetic strips.

By the late 1990s, two-thirds of families had bank-type credit cards. The retail cards where the store, instead of a bank, issued the credit began to wane.

Credit card use plateaued at about 75% for the first years of the 21st century, but then rose to over 4 out of 5 families in the late 2010s.

These days imprinters are utterly obsolete, and our latest credit and debit cards lack embossing. They still have have the magnetic strip on the back for old-style swiping. Encoded on the strip are the credit card number, your name, the expiration date, etc.

Since imprinters are no longer used, credit cards have lost the embossed name and number; the information is instead encoded in the magnetic strip, while the embedded chip can be used for more secure transactions

But in 2015 EMV chips began to be added to the credit cards in the USA, over a decade after they were introduced in Europe and five years after they came to Canada. EMV stands for Europay, Mastercard, and Visa, and using the chip is more secure than the magnetic strip, since it generates a transaction-specific, one-time code that cannot be duplicated ahead of time instead of sharing the actual credit card number.

Most credit cards are still “dip and sign” ones in which you insert the card in the reader, wait for the signal, and then may be prompted to provide your signature, although most card issuers no longer require a signature since signatures are not effective at preventing fraud.

However, some stores still require a signature for transactions over a given amount, have old card terminals that rely on the magnetic strip instead of the chip, and restaurants that lack pay-at-the-table terminals often, but not always, require a signature to validate a tip the customer adds to the merchant slip.

Some expect us to migrate to cards where using the chip in a terminal also requires that you enter a Personal Identification Number, as one commonly must do with bank debit cards. But a newer technology offering better security is preferred: tap-to-pay. A card (or smart phone) with tap-to-pay capability has an embedded antenna.

Modern credit cards have lost the embossing, but gained the EMV chip and a tap-to-pay antenna

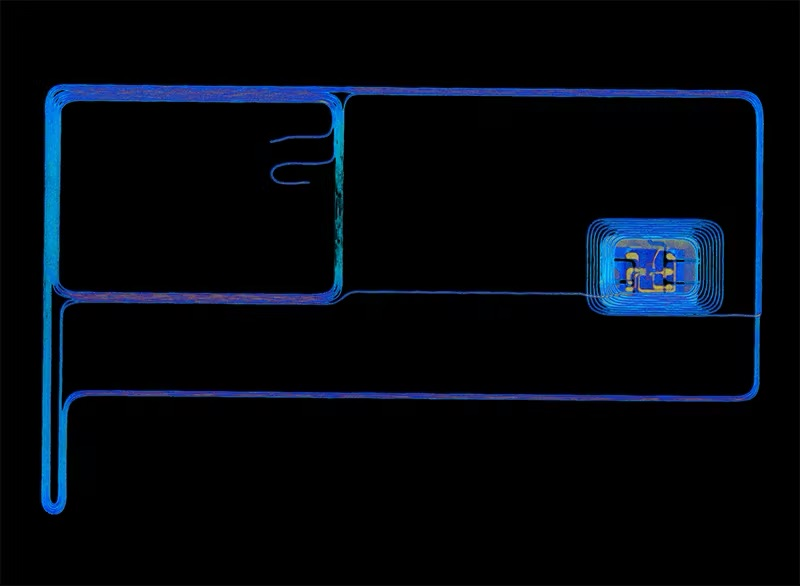

A CT or computed tomography scan of a contactless pay credit card reveals the antenna wires around its perimeter which then coil tightly around the EMV chip.

Tap-to-pay credit cards have antenna wires embedded in them around the perimeter of the card and its EMV chip

When you use tap-to-pay, the pay terminal uses alternating current to generate an electromagnetic field at a frequency of 13.56 million cycles per second. That field oscillates across the wires in the credit card, inducing an electrical current in it to power a tiny integrated circuit in the card. The card rapidly changes its resonance to create detectable fluctuations in the terminal’s electromagnetic field, thus communicating with the terminal.

Like transactions where you insert the card to read the chip, each contactless card payment creates a one-time code and avoids transmitting the actual credit card number. But contactless tap-to-pay is even better since you never have to insert your card in a terminal. That avoids falling victim to a terminal secretly outfitted by criminals with a skimmer that actually reads the magnetic strip to gain your credit card number and other information.

I love the tap-to-pay feature. I even instructed one bank to issue me a replacement card since the new one would have tap-to-pay and that was lacking on the card they had issued me a few years ago. But does the use of radio waves for tap-to-pay mean that crooks could walk by you and scan your credit card?

No. The effective range for tap-to-pay is deliberately designed to be quite short, maybe a few centimeters, and the card doesn’t actually transmit the account number, but instead a one-time code. The risk of electronic pickpocketing is minimal compared to physical card theft. So I don’t bother worrying about wallets that block radio waves.

Plus, in the U.S. there is little if any consumer liability if a fraudulent purchase is made. The real danger inherent to using a credit card is in its name: credit.

As people use credit cards more, the debt associated with them is building even as the personal saving rate, which spiked during the pandemic, has fallen. Bear in mind that the debt is volumetric while the saving rate is a flow, but the contrast in the trends is still interesting.

As the Federal Reserve raised interest rates from March 2022 to July 2023 in order to combat high inflation, that prompted credit card interest rates to spike. Axios reported that in September 2024 the average credit card interest rate was at 20.78%, close to the highest on record, and the current average interest rate on store-branded retail cards is a whopping 30.45%.

Commercial bank interest rate on credit cards plans in the USA from 1994 to 2024; Source

So if you’re not paying off your credit card bill each month, it might behoove you to start using debit cards instead. Merchants prefer them anyway since their processing fees are lower, disputes and chargebacks are easier to handle, and the money is available to the merchant more quickly.

How we pay will continue to evolve. Here’s hoping we can continue to reduce the friction as well as the fraud.

For me, EOL first means End of Line. That is thanks to my interest in computers and the 1982 movie Tron. The computer programs in it would end a conversation thusly:

Back then, the computers I was dealing with indicated the end of a line of text not by a single character or phrase, but instead by the American Standard Code for Information Interchange signals for carriage return followed by line feed. Those were obvious holdovers from the days of mechanical teletypes. Having grown up learning to touch type on a manual typewriter, I was all too familiar with both functions, which were performed on an old typewriter by swiping a metal lever on the left end of the carriage.

Going back even further, telegraph operators used to send the Morse codes for B and T, without the usual pause between the two characters, as a “Prosign” to Break Text, and the Morse Prosign SK, for Silent Key, indicated the end of a transmission.

However, in computing these days, EOL commonly means End of Life: a cutoff date after which a product will no longer be supported. I’ve certainly encountered those over decades of personal computing. As I write this post in September 2024, there are a few EOLs coming up that interest me:

EOL

Effect

October 14, 2025

End of support for the Windows 10 Operating System

August 2027

End of support for Google Pixelbook

2027-2030

Expected end of support for the Apple Mac Mini M1

Windows 10 EOL

Microsoft will no longer provide technical support, security updates, or software updates for Windows 10 after October 14, 2025. That will be a decade after it was initially released, and four years after Windows 11 became available. I’m used to that, as someone who has used Windows since version 1.03 was released in May 1986 and who fully switched from MS-DOS to Windows in 1995. Historically, Microsoft has often cut off support about a decade after a major release.

Windows 11 has no compelling advantage over Windows 10, and my personal Windows 10 desktop and laptop computers from 2017 would probably still be viable in October 2025 except that Microsoft has chosen to not support upgrading them to Windows 11.

Two decades ago, I was able to update a Dell desktop computer purchased in 2000 from Windows 98 to Windows 2000 and then Windows XP, but I haven’t always been so lucky. My 2009 Velocity Micro computer couldn’t handle the shift from Windows 7 to Windows 10.

The Windows 10 EOL is why I directed that all of the desktop computers in our high school and middle schools be Windows 11 machines by the end of the summer of 2024, with the elementary schools and administrative sites to be refreshed by the end of the summer of 2025. The waves of desktop computer refreshes are coming seven years after our previous ones, and none of the computers we bought in that earlier refresh can be upgraded to Windows 11, although some systems we purchased after that can make the transition.

Those will also be the final refreshes I direct for the school district, as I have given my career in the Bartlesville Public Schools its own EOL of June 2026. I’ll be turning 60 in July 2026, and my finances are such that I can feasibly retire as I complete 37 years of service.

I think of my personal timeline like playing a piano keyboard right to left, starting with the highest pitches and working my way to the low notes, possibly getting to play 88 keys across over 7 octaves. The top two octaves were high tinkly notes I played while growing up, I am almost done playing three middle octaves while working at Bartlesville Public Schools, and I hope to play at least a couple of final octaves in retirement.

As I shift from earning a monthly paycheck to relying on a pension and retirement savings, I will need to be strategic in my computer purchases. I used nine different personal desktop computers over the 42 years from 1982 to 2024, so they typically last five or six years for me.

My Next Desktops

I replaced my full-size Windows desktop computer with a little Mac Mini

In April 2024, I decided to replace my 7-year-old Dell XPS 8910, which cannot be upgraded to Windows 11, with an Apple Mac Mini M1 which I had purchased in 2021. I documented that transition in a series of posts. Five months later, I haven’t regretted it.

Over Labor Day weekend 2024, I finally disconnected the big black Dell desktop and stowed it under my desk. I hadn’t turned on the beast in months. At over 15″ tall, 7″ wide, and 14″ deep and weighing in at over 20 pounds, it dwarfs my Mac Mini, which is a square 7.7 inches on each side while only rising up 1.4 inches and weighing a mere 2.6 pounds.

Apple typically supports its computers for six or seven years, so the Mac should outlive the Windows desktop by a couple of years. Thus far, the Mac meets all of my needs, so I can hopefully delay replacing it until after my retirement, and then jump from the M1 to the M5 or M6 microprocessor.

My Next Laptop

I’ve never been a big fan of laptop computers, although I’ve personally owned five of them since 1997, plus several Chromebooks. I much prefer Apple iPads for my portable computing needs, although just after buying my first of seven iPads back in 2010, I bought the first iteration of the MacBook Air. Its thin wedge design still wows me, but I used it very little while using my iPads on a daily basis.

My 2010 MacBook Air

My Microsoft Surface Book

I bought my current laptop, a top-of-the-line Microsoft Surface Book, back in 2017 as I switched from teaching physics to leading the district’s technology efforts. I thought I might need it for my new position, but that didn’t really happen until the spring of 2020.

For the first five months of the COVID-19 pandemic, I used the Surface Book as my primary machine for many virtual meetings. However, I never got my money’s worth out of that $2,600 device, and I never made use of its stylus or found its detachable screen of much use.

When I stowed the big desktop computer away under the desk this month, I moved the Surface Book to a side table in case I need to use Windows at home before October 2025. I fired up that laptop to ensure it still worked and was up-to-date, and I discovered that I hadn’t booted it in a year-and-a-half.

2019: Google Pixelbook

Instead of that Windows laptop, for portable computing I have mainly relied on my Apple iPads as well as a Google Pixelbook Chromebook that I purchased in 2019. I purchased the Pixelbook because I was leading a districtwide shift from Microsoft to Google applications as part of implementing a 1:1 student computing initiative. If you want students to learn with Chromebooks, you first have to get teachers using them, so I ensured that every teacher had his or her own device, and I routinely used one at my various meetings.

One should lead by example, so I also made the deliberate choice to do my word processing with Google Docs instead of Microsoft Word or Corel WordPerfect. I’d been a loyal WordPerfect user since 1986, but it was past time to move on. I also began to use Google Sheets instead of Microsoft Excel for most spreadsheets, and Google Slides instead of Microsoft PowerPoint. I never liked PowerPoint, however, so that transition was delightful.

My nice Pixelbook will reach its own EOL in August 2027, and until I switched to using my Mac Mini as my primary home computer, I presumed I would replace it with another Chromebook. But by then I will be retired, and the Apple ecosystem brings many benefits. So when my Chromebook reaches EOL, I may try just using an iPad with a Magic Keyboard rather than investing my retirement money in another Chromebook. If the iPad just isn’t enough for my portable computing needs, I’ll consider another MacBook Air.

Embracing EOL

I’m already actively preparing for my career EOL. I’m logging my routines and significant daily activities as a potential guidebook for my successor(s) in leading the district’s technology and communications efforts. I’m steadily shifting and sharing digital assets so that my successor(s) can access and support them.

I also enrolled in the Leadership Bartlesville Class XXXIV. That Chamber of Commerce program has introduced me to about 30 other community members. Over the next eight months we’ll spend at least a day each month visiting and touring local enterprises to learn more about private companies, community nonprofits, city government, and local services. I’m among the oldest in our group, and I’ve been clear from the start that I’m learning more about Bartlesville programs so that I am aware of different ways I might participate in community life once my career in public education has concluded.

I am one of those people who tend to misplace items. I’ve donated countless umbrellas and clip-on sunglasses to the world at large, and I hesitate to estimate how often I go squinting around the house, nearsightedly trying to locate my spectacles.

Over time I’ve adapted to this shortcoming. My presbyopia has me donning and doffing “computer glasses” that are just full-frame renditions of the reading prescription part of my bifocals. So on my desks at work and home, as well as beside my bed and recliner, I have plush lined eyeglass holders. They have reduced, but hardly eliminated, my squinting perambulations.

To further reduce the problem, I have contemplated removing the window sills from our home, along with all of the tables, counters, shelves, and any remaining flat elevated surfaces. My wife, Wendy, countered that I might instead keep my regular spectacles on a cord or chain about my neck, which is far too practical a solution for my taste.

I stepped outside with a hand over one lens to get this shot

Unwilling to shell out the dough for prescription sunglasses, for years I would regularly buy, and lose, clip-on sunglasses at Walgreens. Recently I decided to return to larger lenses, which presented the opportunity to finally try photochromic lenses that darken when exposed to ultraviolet light.

They have dyes in them with chemical bonds that are broken by higher-energy ultraviolet light, changing the shape of the dye molecules to ones which absorb more visible light.

I love them, but they do tend to have a slight tint when worn indoors. Wendy puts up with them, although she associates tinted lenses with “creepers”, so she prefers my computer glasses. I can’t criticize her take too much, as I still stereotype tattoos as being for sailors, carnies, and criminals, although I realize how unlikely it is that one of out every three Americans fits one of those categories.

Six backup umbrellas might be enough for awhile

As for umbrellas, I just went out to my car and counted. There was one little umbrella in the driver door and six larger ones in the trunk, ready to be left behind in restaurants on rainy days. Our rainstorms just don’t last long enough for my protection.

This week I needed to replace a bunch of huge air purifier filters in the auditorium and Bruin Field House at the high school. I decided to take along a screwdriver to help me wedge open the large metal covers.

I opened my office drawer and grabbed the little screwdriver I made in college.

The screwdriver I made back in college; the stamped initials were important

I crafted it in a physics lab class, cutting a steel rod and tapering it. I knurled the end that would get inserted into the wooden handle, stamped the blade with my initials, and then I hardened it. That involved heating the steel up until it was past the Curie point where it lost its ability to be magnetized. Then I quenched it, dipping it into saltwater brine to rapidly cool it.

The next step was to temper the steel since the hardening process also created internal stresses that made the blade more brittle. The tempering was a second heating to a lower temperature after which I allowed it to cool at room temperature. That restored some of the steel’s ductility.

As for the handle, it was a wood dowel. I bored a hole in the center for the blade and sanded the dowel into an octagonal shape with chamfered edges, then stained the wood and drove the knurled end of the blade into the handle along with some epoxy glue.

The most important step in that process was stamping the blade with my initials. That ensured, almost 40 years later, that my little screwdriver was later returned to me a few days after I inevitably left it somewhere in the high school during the filter replacement process. The stamped initials also helped it appear less like a shank and more like a tool.

Speaking of tools, one of the times I was in British Columbia I of course managed to lose my passport card. They used to just let you drive or ferry across the border with a driver’s license, but later you needed a passport or a cheaper passport card. I didn’t realize I’d lost my card until approaching the border, and I took my chances.

I explained the situation to a border officer, offering my driver’s license and a rueful smile, although I thought about widening my eyes and holding my hat for a Puss in Boots sympathy win. He waved me through, telling me to be sure to file a report on the lost card. Being a good, albeit forgetful, fellow, I did just that.

If I can’t donate an umbrella, I sometimes leave my wallet at a restaurant. I have a habit of leaving it out on the table after I hand over my credit card to the wait staff, supposedly to remind me to wait for the credit card’s return. Wood-grain tabletops are my nemesis, as my leather wallets blend right in with them, especially since I’ve no doubt doffed my spectacles.

I remember leaving a wallet behind at the Spaghetti Warehouse in downtown Tulsa back in the 1990s. I didn’t realize it until I was ensconced in a three-hour-long graduate class miles away. Needless to say, I was distracted throughout the long class, and I drove very carefully back to the restaurant afterward. The wallet was retrieved, and the finders had helpfully emptied it of all the cash as their reward, saving me the trouble.

I’ve also left my wallet at the local Chili’s before, but they returned it without bothering to take the cash. In fact, when I ate there once and realized I had forgotten my wallet somewhere else (this was before smartphones and tap to pay), they said the meal was on them and they looked forward to my return. It pays to live in a small city.

Speaking of cash and smartphones, my latest wallet escape was last week. This time I completely struck out on locating it, which was thankfully the first time, out of many, that I didn’t eventually retrieve it. Wendy was alarmed, but I’m so used to being an absent-minded fool that I took it in stride. It didn’t take long to cancel the five debit and credit cards, and I already had a spare driver’s license in the car…you know why.

Apple Card saved the week(s) when I lost my wallet

Thanks to modern living, losing the cards in my wallet wasn’t a hassle, even though as I write it has been over a week and so far only one of my replacement cards has arrived: my new Apple titanium card. Ironically, that was the only physical card that I had never used.

I did fine without any physical cards, as I was still able to use the Apple Card tap-to-pay feature of my iPhone without a wallet, and my Amazon credit card has no corporeal existence, so it couldn’t be lost. I also had some emergency cash in the car…again, you know why.

For years, I loaded these coins into my pocket each morning

The pandemic broke my old daily habit of loading a pocket each morning with four pennies, a nickel, two dimes, three quarters, and two gold dollar coins. A coin sorter still sits on the counter where I place my keys and wallet, but all of the coins are just gathering dust.

I just don’t use cash much anymore, similar to how I seldom write any checks. I used to regularly visit an automated teller machine to withdraw $100 and later $200 in twenties. Then Arvest changed one of their ATMs so that if you withdraw $200, instead of ten Jacksons you get a Benjamin, a Grant, and a mix of Jacksons, Hamiltons, and Abes. That, along with the increasing adoption of tap to pay, led me to abandon using cash for most transactions. Sorry, wait staff!

One of the ATMs has become more diverse, although they are all still dead white guys

Losing my wallet did have one happy outcome. For years Glide Apps charged one of my credit cards $25/month for some “legacy” apps I wrote for the school district back when their service was free. I just paid the bill since the service won’t take purchase orders.

Then the legacy service lost a needed feature, so I went through the process of recreating the apps in their new service. Given the effort involved, I threw in working through paying for the new service via a school district credit card. However, repeated attempts to get Glide to stop separately billing me for the legacy apps had been stymied.

So I grinned broadly this week when they started sending me complaints that they could no longer charge me $25 since my credit card was no longer valid. Aw, that’s too bad, ya ninnyhammers!

As for preventive measures against future losses, Wendy suggested I get a bright pink wallet, as none of the victual houses I frequent are adorned with pink formica tables. I instead opted for a high-tech solution, ordering an Ekster Tracker Card.

Supposedly that rechargeable device, which is as thick as two credit cards, will give my phone a left-behind alert, has a 95 dB ringer, and can be tracked with the Apple Find My app. I can’t wait to lose it!

Having enjoyed several walks in the redwoods, it was time to head back to Medford so that we could catch a flight back home. We packed out of Elk Meadow Cabins and began retracing our route along US 101.

We turned off 101 after Crescent City to rejoin US 199, the Redwoods Highway, which led through Hiouchi and Gasquet onward to Cave Junction. The road is particularly narrow and winding east of Gasquet, and I was glad when, three hours after departing our cabin, we reached Cave Junction.

Back in 2006, I had turned off here to see the Oregon Caves National Monument. However, Wendy and I have been through several caves, and she was content to skip them on this trip.

Cave Junction sits in the Illinois Valley, which had a gold mining boom from the 1850s into the 1870s. As the gold played out, Elijah Davidson found a cave on a hunting trip in 1874. The Oregon Caves were a tourist attraction in the 1890s and converted into a National Monument in 1909, with a chalet and cabins in place by 1926 when Cave City was established at the junction of the Redwood Highway and a branch leading to the caves. It became Cave Junction in 1935.

The town has now surpassed 2,000 and offers the only restaurants and public restrooms I saw after Hiouchi. We had lunch at the River Valley restaurant, which had good food and service, although I wish its dining room had some acoustic dampening.

The remainder of the trip back to Medford was relatively quick, especially once we joined Interstate 5 at Grants Pass. After about an hour, we had reached the Crater Rock Museum in Central Point, just north of Medford.

Crater Rock Museum

Frieda and Delmar Smith founded the Crater Rock Museum in 1954. It grew from a small shed into what is now a 12,000 square foot facility. Wendy enjoyed browsing the large shop. Then we paid $13 ($7 for her and $6 for her “senior citizen” hubby) for admission to the museum.

Frieda and Delmar Smith

As one might expect, there were some small children enjoying the exhibits, and Wendy was glad to have earplugs to dampen the louder yammerings of toddlers.

The first displays we saw had some 19th century sand paintings and ivory carvings.

After that, we saw many varied rocks. Here are Wendy’s favorites:

Then we drove south into Medford, relaxed with some ice cream at a Dairy Queen, and then checked into the Homewood Suites by Hilton.

Our suite was the most comfortable of the trip, which made up for how it was situated on the second floor at the farthest back corner of the property. I figured out how to use the courtyard as a shortcut to and from the lobby.

We’d noticed some Asian restaurants on our drive through downtown, and I ordered us a meal via Grubhub from Dragon Express, which was pricey but good.

We had a day to kill before flying out on Monday, so on Sunday we filled up the rental SUV with gasoline, shopped at a nearby Fred Meyer’s, ate at a Five Guys, and I bought Wendy some baklava at the Harry & David store.

Baklava from Harry & David

Harry & David was established in 1914 and specialized in the Comice pears grown in the area. They became a premier marketer of fruit and food gifts and one of the nation’s oldest catalog mail-order companies. Harry & David is still one of the largest employers in the Rogue Valley.

We were introduced to the company via a Christmas gift a few years ago from Truity Credit Union back when I served on their Technology Committee. Wendy loved the baklava in that gift assortment, so it was fun to visit the home of Harry & David and purchase some in their store rather than via mail order.

Their baklava is made by buttering 60 paper-thin leaves of phyllo pastry with intermittent layers of a filling made from Sumatran cinnamon and finely chopped and toasted English walnuts. The confection is baked until golden and flaky and then bathed in honey and lemon. Wendy loves it.

On Monday we checked out of the hotel, dropped the SUV off at the airport, and had lunch in its second-floor Sky House restaurant. I was glad we did, as I didn’t particularly care for the lunch served later on our flight to Denver, although we both liked the warm Chocolate Chip Cookie Pie in the Sky treats we were served.

We again enjoyed carefree flights home, although we both came down with COVID after our return, making us wish that we had masked up while at the airports and aboard the planes. Those high-risk environments were most likely where the latest variants caught us.

I visited the Pacific Northwest in 1998, 2005, 2006, 2008, 2009, and for our honeymoon in 2016. This seventh visit was again rewarding, and I am certain we shall return to the region to escape some future summer in Oklahoma.