I was asked to share information about Teacher Retirement at our school district’s Leadership Day after the conclusion of the 2023-2024 academic year. My own retirement is a couple of years away, so I enjoyed doing some research about the topic. I’m sharing some of my findings and personal experiences here for anyone who is interested. Bear in mind that I am certainly not a qualified financial advisor; I’m a former physics teacher and current school district administrator who knows how to use the internet.

Deciding when to retire

While the average over-50 worker expects to retire at 67, and 2/3 of older employees plan to retire after 65, the average retirement age in the USA was 57 back in 1991, rising to 59 by 2002, and it has averaged 60 to 62 for over a decade.

The truth is that many people don’t get to retire when they want. Annual surveys show “…actual retirement tends to arrive abruptly and unexpectedly, triggered by declining health or corporate downsizing.”

More than half retired earlier than planned, for a variety of reasons, most often for health or job-related reasons.

My mother retired at 54 and my father at 58 when their respective corporate employers were sold. Neither of them earned income after they retired.

In an EBRI survey, 3/4 of workers expected to continue working for pay in retirement, but only 3 in 10 retirees had ever done so. In an AARP survey, “over three in five (64%) believed workers face age discrimination in today’s workplace and few see the situation improving. And, two in five (41%) report experiencing some type of ageism at work in the past three years.”

Since over 2/3 of retirees will not be working for pay, it is important to understand retirement income sources. More discrepancies between worker expectations and retirement realities are apparent in the chart below, with workers underestimating how much of their retirement income will come from Social Security and overestimating how much will be from workplace and individual retirement savings and working for pay.

Social Security is a retirement income source that most workers tend to envision as minor, while 2/3 of actual retirees find it to be major. Over half of workers think workplace retirement savings plans will be major sources of retirement income, but only 1 in 5 of retirees find it to be so. Work for pay is a major source of income for only 1 in 20 retirees, and so forth.

Social Security

Social Security became law in 1935, with payroll tax collections beginning in 1937 and benefit payouts beginning in 1940. There are some common myths about the program, including that is was raided to help with the national debt, while in fact the Social Security Trust Fund was created in 1939 and has always worked the same way. It has never been part of the general fund of the government. The confusion arose because from 1969 to 1990 the trust fund was included in the “unified budget”, but whether or nor trust funds are “on-budget” or “off-budget” are questions of accounting practice that have no effect on the trust fund operations.

Increasing life expectancies and changing birth rates inevitably impact the program. It was heavily amended in 1983 when I was a junior in high school. Those changes helped stabilize it for a half-century. The full retirement age of 65 was adjusted to advance to age 67 for people like me who were born after 1959. The early retirement age of 62 was retained, but the consequent benefit cut was increased from 20% to 30%. Benefits for those with higher incomes were taxed, with the proceeds going into the trust funds, and in 1993 that taxation was increased.

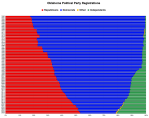

Here is the age distribution of new retired-worker Social Security beneficiaries in 2021:

Almost 3 in 10 took Social Security as soon as they could, and almost half took it before the full retirement age of 65 for those born before 1943. There was a surge taking it at age 65, which is still when Medicare begins, since it is considerably cheaper than private health insurance.

About 1 in 4 took Social Security at age 66, which was the full retirement age for people back in 2021. I expect that surge to shift to age 67 in 2027. Less than 1 in 5 waited past full retirement age to draw their benefits, even though the monthly benefit is increased by 8% for each year of delay up to age 70.

Inflation erodes fixed retirement income sources

The biggest advantage to Social Security over some other retirement income sources is that its benefits are not fixed amounts. Instead, they are adjusted annually to compensate for inflation. Below is a chart of the annual inflation rate over my lifetime:

That includes the “great inflation” period from 1974 to 1982. Inflation was finally brought under control by Paul Volcker of the Federal Reserve, who led the raising of the federal funds rate to a peak of 20% in 1981. That impacted construction, farming, and industry and triggered a recession, but inflation was tamed. The only significant outbreak since then was the post-pandemic peak of 8% in 2022.

Inflation inexorably erodes the spending power of fixed retirement incomes. From 2000 to 2024 the average annual inflation of 3.5% allowed the cost of all goods and services to grow by 85%.

As shown in the chart, medical care costs rose even faster, at an average annual rate of 4.9% for a cost increase of almost 120% over that time period.

As of this writing, the Federal Reserve’s forecast is for an inflation rate of 2.5% over the next 30 years.

How long will you be retired?

The average person’s length of retirement has increased over time. For men, it grew from 13 years in 1970 to almost 19 years today, while for women it increased from 17 years in 1970 to over 21 today. Inflation of 3.5% could erode the purchasing power of fixed income sources by almost 50% over the length of the typical retirement.

However, actual retirement length can vary widely. My father had a retirement that lasted about 38 years, and my mother is currently in independent living at Green Country Village, and she has been retired for about 33 years. The John Hancock and Northwestern Mutual calculators say I have about a 50% chance of a retirement that lasts 28-30 years, but it is of course all just probabilities.

Social Security’s uncertain future

Happily, since 1975 Social Security has had an automatic annual Cost-of-Living Adjustment (COLA) based on the Consumer Price Index for Urban Wage Earners and Clerical Workers. So it is protected against inflationary erosion.

Unhappily, by 2033 or so, the reforms of 1983 will have run their course in propping up the system. With the larger baby-boom generation retiring, costs began to exceed income for the Old-Age, Survivors, and Disability Insurance Trust Funds in 2021. Without reforms, the Old-Age and Survivors Insurance Trust Fund will be exhausted around 2033 and all Social Security retirement benefits would then be cut by about 20% as it would rely on a pay-as-you-go basis using only incoming payroll taxes.

I am one of the oldest members of Generation X, and my full retirement age of 67 in 2033 is when the trust fund will be exhausted. All three branches of our government have become so partisan and dysfunctional that I am dubious that there will be intelligent and reasonable adjustments to increase payments to the system that might avoid at least some significant benefit cuts for younger generations and/or an erosion of the systems’ COLAs.

Even if Social Security were reformed in a way that did not impact me, it might be only 1/4 of my overall retirement income, the majority of which will come from my teacher pension with a substantial boost from defined contribution plans I have contributed to throughout my working life. I delve into those later in this post.

You should get an annual Social Security statement with your projected benefits, or you can access it at ssa.gov. My benefits would be cut by 14% if I start them at age 65. They would be cut by 30% if I start them at age 62. When I take them will depend on when Wendy decides to retire and how comfortable I am living on my teacher retirement and the income I derive from defined contribution plans I have funded.

Insurance before age 65

A major issue to consider for retirement is health insurance. As Oklahoma teachers, Wendy and I each receive HealthChoice High Medical insurance at no cost while we work for the public schools. When I retire before age 65, I will have to pay to stay on that plan along with my HealthChoice Dental plan, and medical costs typically inflate at 5% per year.

If you’re part of HealthChoice, you can get more information at oklahoma.gov/healthchoice.html and as I wrote this post, the HealthChoice premiums could be found at the OMES Employee Group Insurance Division website. Why you can’t find the premiums at the HealthChoice website is another example of how Oklahoma state government is dysfunctional, under-resourced, and poorly managed.

By staying with HealthChoice, the Oklahoma Teacher Retirement System (OTRS) will reimburse about $100 of my health insurance cost each month until I go on Medicare, so my projected monthly health insurance costs until I am 65 would consume about 1/3 of my monthly Social Security benefit, dropping to about 1/5 once I begin Medicare.

Medicare

When I do reach age 65 and go on Medicare, I will have a choice of Original Medicare or Medicare Advantage (which is also called Part C).

Consumer Reports reviewed the pros and cons of each. While Medicare Advantage often has lower monthly costs and enrollees often receive more preventive care, if you have chronic conditions or significant health needs, Medicare Advantage has risks you should consider.

With Original Medicare, you usually have access to a larger network of health providers, and Medicare Advantage plans may require pre-authorization to see specialists. About half of all Medicare Advantage enrollees pay more than those in Original Medicare for a seven-day hospital stay, and Medicare Advantage is problematic for those in rural areas, where the smaller network of providers makes it harder to make appointments and get care.

Here is Consumer Reports’ take on things:

Medicare Advantage’s share of Medicare enrolles has been steadily climbing, and now more than half of the eligible Medicare population are enrolled in it. However, in 2023 only 1/3 of those eligible in my county were enrolled. [Source]

Personally, I associate Medicare Advantage, which is more profitable for insurers than their other lines of business, with managed care and Health Maintenance Organizations (HMOs). I plan to instead piece together my coverage via Original Medicare Parts A, B, and D plus Medigap, along with my existing HealthChoice Dental plan and cancer policy.

Part A, for in-patient hospital and skilled nursing care, should be free. I’ll pay a premium for Medicare Part B, which covers doctor services, outpatient care, and durable equipment. I will also want a Medigap plan for copays, Medicare Part A deductibles, and wellness, but people my age cannot access Medigap plans for vision, dental, hearing aids, or Part B deductibles.

I will have to research my options when I approach age 65, but if I were making the decision today, I might enroll in AARP’s Medigap Plan G. There is also a G+ plan with wellness benefits, but my dentist is not in their Dentegra network for that, so I plan to just stay on HealthChoice Dental for the long term and stick with G instead of G+. But someone with retirement experience has shared that they were happy to be on Plan N from Mutual of Omaha. Definitely do some research before you pick a Medigap Plan!

As for prescription drugs, you can input your routine medications and check costs for various Medicare Part D prescription drug plans at both AARP and Medicare itself. My cheapest option, after I input my medications, was the AARP Part D plan with Walgreens and UnitedHealthcare, but of course your location, preferred pharmacies, and routine medications will cause all of that to vary.

I am increasingly frustrated having to go to a local pharmacy for refills, so I’m currently trying Amazon Pharmacy for my routine medications for chronic conditions.

If you are willing to take the risk, you can research the various Medicare Advantage plans, but bear in mind that if you go that route and later switch back to Original Medicare, you will no longer be guaranteed access to a Medigap plan.

Currently, my estimates are that my monthly insurance costs under Original Medicare with Part A, Part B, Part D, and Medigap, plus HealthChoice Dental and my cancer insurance, would be about 40% lower than my monthly insurance costs from ages 60-64 when I plan to be retired yet ineligible for Medicare. If I took Social Security at age 62, I would expect health insurance to consume 33% of it for three years, declining to 20% once I could join Medicare.

Defined contribution and defined benefit plans

It is only because I have significant sources of retirement income besides Social Security that I can contemplate retiring as I turn 60. In my case, I have both a defined benefit pension plus defined contribution plans I have contributed to throughout my career, although I have no employer matches for the latter.

There was a time when many workers had defined benefit plans, such as the typical pension, guaranteeing a certain payout throughout retirement. However, many businesses abandoned offering pensions, opting to instead sponsor defined contribution plans where money is deposited into an account, but the amount of the eventual payout may not be guaranteed.

401(k) plans, along with their 403(b) counterparts for health care, education, and tax-exempt organizations, are common examples of defined contribution plans. In some cases, the employer will match some employee contributions to a plan.

There is a stark difference in access to the different types of retirement plans for those who work in private industry versus those working for state and local governments:

Access to a defined benefit pension has become a key feature in recruiting and retaining state and local government workers since their salaries are often significantly below what could be earned in private industry. I am among the 34% of state and local government workers with access to both a defined benefit pension as well as defined contribution plans.

Early in my career, the Oklahoma Teacher Retirement System (OTRS) that funds my defined benefit pension was severely underfunded. It was put on a path to solvency by increasing required contributions and essentially eliminating cost-of-living adjustments. There have only been two COLAs for it since 2008, averaging out to maybe 0.25% per year, which is a tiny fraction of the inflation rate. Politicians have sometimes proposed eliminating defined benefit plans for teachers, replacing them with defined contribution plans as has happened to most private industry workers. However, without younger workers contributing to OTRS, the state would have to raise taxes to keep its promises to those still in it. That poison pill has protected the system thus far.

Meanwhile, only 15% of those in private industry even have access to a defined benefit plan, while over half only have access to defined contribution plans. Over 90% of private companies will match employee contributions to a 401(k) up to a certain amount, most commonly capped at 6% of the employee’s salary. The equivalent to private industry 401(k) plans for those working in public schools, churches, and other tax-exempt organizations are 403(b) plans. The funny names come from the tax code.

OTRS

The scarcity of COLAs means that a pension from the Oklahoma Teacher Retirement System is essentially a fixed amount these days. The beneficiaries lack the political power to obtain more than an occasional token COLA. So if you are an OTRS member looking at your projected pension amount, bear in mind that its purchasing power will steadily erode by perhaps 2.5% or more each year, or perhaps by half over the length of a typical retirement.

Getting more accurate projections

Speaking of OTRS projections, the annual statements the OTRS mails out are not useful if, like me, you want your spouse to continue to receive all or part of your pension should you die first. That’s because the amount of your benefit depends on how long your spouse is expected to live. To get an accurate projected benefit for “Option 2” or “Option 3” to provide a spouse with all or half of your pension if they survive you, you need to go online and select the Retirement Projection option at My OTRS:

There you can put in your spouse’s birthdate if you want Option 2 or Option 3 surviving spouse benefits.

That same Options page is where you can input any unused sick leave you will have at retirement, which purchases you additional credit in OTRS and increases your benefit. The maximum increase is with 120 days of accumulated sick leave, which provides a full year of additional credit. In my case, that translates to about $2,000 per year more, or about $50,000 over the length of my projected retirement.

Of course, another factor is when you expect to retire. Over time, the age at which you could automatically receive full benefits from OTRS has increased from 62 to 65. Some can qualify before those ages if the sum of their age and years of creditable service is at least 80 or 90. They’ve also tweaked the amount of benefits you can receive if you retire early.

| Rule of 80 | Rule of 90 | Rule of 90 Revision | |

| Those who joined… | prior to July 1, 1992 | between July 1, 1992 and October 31, 2011 | after October 31, 2011 |

| Full retirement age | Age 62 | Age 62 | Age 65 |

| Service & age combination if below retirement age | Age + Years of Creditable Service = 80 | Age + Years of Creditable Service = 90 | Age + Years of Creditable Service = 90 and at least Age 60 |

| Early retirement amounts | 100% at age 62 declining to 56% at age 55 | 100% at age 65 declining to 80% at age 62 and 65% at age 60 | |

| Benefit calculation | Highest three salaries | Highest consecutive five salaries | |

Salary caps for service before July 1995

I joined back in 1989, so I am under the Rule of 80. But that also meant that I made an election in August 1989 of whether to have my salary cap for OTRS set at $25,000 or $40,000. I was only making $17,657 per year starting salary, which would be equivalent to $44,433 in 2024 if adjusted for inflation.

I opted for the $40,000 cap, so when I qualified for full OTRS retirement in 2018 under the Rule of 80, my benefit was reduced because it was calculated as 2% of the average of my three highest salaries only for the years 1996 and beyond. For 1989 through 1995, it was calculated using 2% of $40,000.

To encourage Rule of 80 folks like me to not retire so early, the “Education Employees Service Incentive Plan” eliminated two years of the salary cap for each year I stayed beyond my eligibility year. So after July 2021 I had worn away the old salary caps for my first six years in the system. The confusing statement from OTRS still acts like my old salary caps are in place, but when I run the calculations, its projections are correctly based on my having no caps any more.

Coupling OTRS & Social Security

To gauge how OTRS and Social Security could fund my lifestyle if I retired at various ages, I divided my projected benefits, as well as my projected insurance costs, by my current taxable monthly wages.

To get a more accurate handle on things, I also backed out, with negative percentages, my expected health insurance costs. Here are the results:

A common rule of thumb is that you should aim to replace 80% of your pre-retirement income in retirement. So retiring at 60 on just my teacher pension would not be comfortable. Things would be better once I could start collecting Social Security. Waiting to retire until age 62 would allow Social Security & OTRS to replace 100% of my current taxable income, while retiring at 60 would reduce my OTRS such that when I reached 62 and could start Social Security, together they could replace 95% of it. Bear in mind that in all scenarios, inflation eats away at the purchasing power of my pension.

Some people go to the trouble of calculating, based on their life expectancy, their net lifetime retirement benefits if they delay starting Social Security to various ages, but remember that over half of retirees take it before reaching their full retirement age.

The reason I am comfortable retiring before I qualify for Social Security is that for my entire adult working life I have been contributing to optional defined contribution retirement plans.

Defined contribution plans

As a member of Generation X, I knew that I was unlikely to enjoy the same Social Security benefits as my parents, who were of the Greatest Generation and the Silent Generation. I figured that the immense Baby Boom Generation, with its sense of entitlement and political power, would protect itself while cutting benefits for us in Generation X and the later Millennials and Generations Z and Alpha.

So I began contributing to an Individual Retirement Account (IRA) when I started teaching in 1989, and I started contributing to a 403(b) annuity plan in 1992. 403(b) plans are like 401(k)s in which your contribution is usually deducted from your paycheck from pre-income-tax dollars, so your eventual benefits are subject to income tax. Traditional IRAs work similarly.

Roth IRAs became available later, where you could only input after-income-tax money, but your earnings and eventual withdrawals would not be subject to income tax. Roth IRAs also have fewer penalties and restrictions on early withdrawals.

There are also 457(b) plans, multiplying your options. Below is a chart I made comparing the different plans, but remember, I’m not a financial advisor:

So how many people take advantage of these plans? In a May 2023 Yahoo Finance survey, 37% of retirees have no savings. An AARP survey in April 2024 found 20% of adults ages 50 and older had no retirement savings.

The Census Bureau reported that in 2020 18% of working-age individuals had IRA or Keogh Accounts and 35% had 401(k), 403(b), 503(b), or Thrift Savings Plans.

As for those who have savings, here are the medians for each age group in 2022:

- Under 35 years: $18,880

- Age 35-44: $45,000

- Age 45-54: $115,000

- Age 55-64: $185,000

- Age 65-74: $200,000

- Over 75: $130,000

The old 4% rule says that a person with $185,000 in savings might be able to draw $617 per month for retirement and keep up with inflation. That’s far less than my Social Security benefit, let alone my teacher pension.

So this cynical Gen-Xer made decades of sacrifices to bolster his retirement income. I will caution, however, that I also never had children and was an only child of generous middle-class parents. So I had the opportunity to save more than the typical head of household, even during the 28 years I was earning an Oklahoma teacher salary, before I became a higher-paid administrator. I will also note that my salary has always been a fraction of what I could earn in private industry; thank goodness Oklahoma has a very low cost of living.

Fiduciaries versus financial advisors

Before I go any further about investments, I will also caution that if you are seeking advice about investments, including defined contribution retirement plans, be sure you understand the differences between fiduciaries and financial advisors. A fiduciary has a legal obligation to act for the beneficiary’s benefit and not their own, while the title “financial advisor” implies no legal obligation. Certified Financial Planners and Chartered Financial Analysts are fiduciaries who must avoid conflicts of interest, but that also means you may have to pay up front and/or higher fees for their services, versus some financial advisors who make money by selling products that might not be in your best interest.

Types of investments

There are many types of investments. As I have repeatedly warned, I am not a financial advisor, so take my summary chart below with a grain of salt:

CDs

When I was young, some CDs still had high interest rates as a result of Volcker’s battle to tame inflation, and they are very safe investments. I had some for my personal savings and I also invested my Traditional IRA in them, despite their faltering interest rates. When I bought my home in 1994, I cashed all of them out except for the ones in my IRA.

My Traditional IRA was originally with Liberty Bank, but they eventually shifted it to Bank of America, which then shifted it to MBNA, which eventually shifted it to Commercial Bank out of Parsons, Kansas. I wasn’t at all happy with the interest rate there, so in 2016 I consulted a financial advisor and shifted the money into a Nationwide New Heights 9 annuity with an income rider…in other words, a way to simulate a smaller additional pension.

Annuities

The Traditional IRA I contributed to from 1989 until 2016 is now set up for a joint fixed income annuity, which can be thought as a way to finance your own fixed pension by buying a policy from a large, stable insurance firm. Your investment compounds over the years and, upon retirement, the firm uses your invested money and actuarial tables to calculate a fixed amount they will pay to you, or if you’re like me and buy a joint life annuity, they will pay to you and then to your spouse if they survive you.

I was interested in annuities because I worried about outliving my savings if I instead invested and just used the old 4% rule. My paternal grandfather lived to age 100, my father to age 97, my paternal grandmother to age 91, and my mother is still living in an independent living facility at age 87.

I have always been able to control which funds the 403(b) plan was invested in, so I could alter the ratio of stocks versus bonds, the size of companies I was indirectly investing in (large, medium, or small-capitalization), and how much was invested in foreign versus domestic companies.

Stocks

One rule of thumb is that stock-based investments average 9-10% annual returns while bonds average 4-5%. The reason one invests in bonds, despite their lower returns, is that they are far less volatile than stocks. A stock, as well as a stock index based on a large number of stocks, can rapidly rise and fall, and individual stocks can become worthless.

I’m certainly not a fan of investing in individual stocks. Back in the early 1980s, my father invested some money in the stock of a new hog finishing operation in Lexington, Oklahoma called Sooner State Farms. Its stock price dipped from a high of $1.38 per share to only 31 cents by April 1985. Dad gave me $7,500 in stock in 1989, and I watched it crash to $1,800 within a year. I sold all of my stock in 1995 and from then on only invested in managed or index funds that were a mix of equities from many companies, as I had no interest in tracking the stock market, let alone trying (and failing) to outperform it.

Investment mixes

With my Traditional IRA invested in low-risk and low-return CDs, when I began contributing to a 403(b) in 1992, I opted for higher returns, which meant higher volatility. In general, my approach was to keep a majority of the funds in balanced funds and/or stock index funds. Index funds outperform the typical managed fund.

Volatility and dollar-cost averaging

I’ve certainly seen volatility in my 403(b). There have been three recessions over its lifetime. The recession of 2001, triggered by the dot-com bubble burst, dropped my account’s compounded value below the inflation rate for four years. Then the Great Recession of 2008, triggered by the housing bubble, dropped it below inflation for over five years.

But I was still far from retirement, so I trusted in dollar-cost averaging, where you continue to invest steadily through booms and busts. Over the long haul, continuing to invest when the market is poor eventually pays off in what you’ll own when stocks recover. You just have to not panic.

The first recession led to annual returns for my account in 2000-2002 of -10%, -18%, and -22%, while the Great Recession wiped out 40% of its value in 2008. It also lost 19% of its value in the post-pandemic recession of 2022. But I just kept steadily investing, and over its lifetime my 403(b), despite my lack of investment expertise, has had an overall lifetime return of between 6% and 7%.

Roth IRA

When I rolled my Traditional IRA over into the fixed annuity investment, I started a Roth IRA. Those first became available in 1998. Unlike Traditional IRAs and traditional 403(b)s, your contributions to them are not tax deductible, but the earnings and withdrawals are tax free. The usual advice is to invest in a Roth if you expect your tax rates will rise, either because your wealth and income will be higher when you retire or due to expected changes in tax law.

Since most of my retirement savings was in pre-tax vehicles, I liked having some in a Roth, and I appreciated how it has no minimum distribution rules. One can only contribute earned income to a Roth, but since Wendy and I file a joint married tax return, I can still contribute to my Roth after I retire for as long as Wendy, who doesn’t contribute to an IRA and is younger than me and under the OTRS Rule of 90, chooses to continue to work.

How much to save

Most financial experts recommend a retirement savings goal of 10% to 15% of your pre-tax income, but whether or not that is feasible depends on your income, lifestyle, general cost of living, and the big expenses of children, housing, vehicles, and vacations.

I was fortunate to be able to contribute the maximum to my IRA each year, whether it was a Traditional or a Roth, including the larger “catch-up” amounts available to me once I was older. Over the past 35 years, my IRA contributions have averaged at 9% of my gross salary.

My annual contributions to my 403(b) averaged at 10% of my gross salary. I increased my monthly contributions to it in 1993, 1997, 2015, 2018, 2019, and 2024.

So over the years I’ve put 19% of my gross salary into voluntary defined contribution retirement plans. But many of my colleagues have not been so fortunate, with some not having defined contribution plans while others had one but then raided it when a life crisis occurred.

Spouses

Throughout retirement planning, if you’re married, you must take into account your spouse’s situation, especially with any differences in age, retirement, or insurance plans. I’ve concentrated on my own retirement situation in this post, but behind the scenes I have also run various scenarios based on Wendy’s situation. Since she is nine years younger than me, she won’t even qualify for a reduced OTRS benefit until several years after I retire, and her Social Security and Medicare eligibilities arrive almost a decade after mine.

Our Plan

I’ve met with my financial advisor and she has developed an initial plan for our retirement income. We will revisit that plan periodically to see if anything needs adjusting. A large uncertainty is when Wendy will choose to retire, so I will be opting to increase our flexibility by taking a partial lump sum from my teacher retirement. That will decrease what is essentially my fixed teacher pension while increasing the funds I can choose how to invest, increasing my options on when and how much of those funds to utilize for income.

If you are still working and this post has you thinking about your own retirement plans, I will count that as a success. Please do not interpret this post as personal or financial advice; everyone’s situation is different, and if you are looking at investing, I would advise you seek out a Certified Financial Planner who is also a fiduciary.